Subprime customers—or those who don’t have established credit scores—aren’t typically the type of customers retailers pursue. After all, how can you be sure that they a) can afford your product or service and b) are worth investing in for the long-term?

However, a report from TransUnion found that only 50% of Gen Zers have credit cards and have a utilization rate of just 31%. What’s more, according to Jim Wang, the founder of financial advice blog WalletHacks, “It can take upwards of ten years for most individuals to fix their credit scores after making a mistake when they’re young.”

We’re here to tell you that subprime customers pose an excellent opportunity for merchants to increase revenue and build lasting and mutually beneficial customer relationships. But how?

In this article, we cover:

- What are subprime customers?

- What is a buy now, pay later payment method?

- The benefits of using a buy now, pay later option to empower customers financially

What are subprime customers?

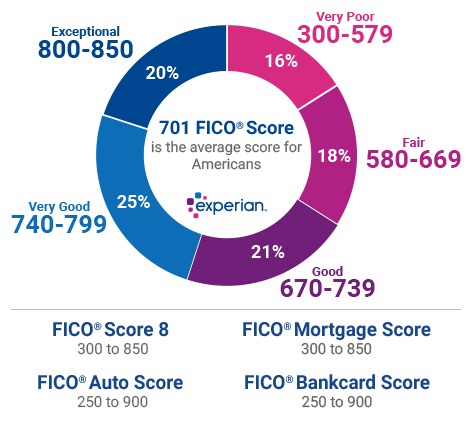

Subprime customers are likely to have a hard time repaying debts or loans based on their credit history and FICO score. According to Experian, a FICO score between 580 and 669 is considered “fair” or below average.

(Source: Experian)

If you have a higher credit score, it’ll be easier to get approved for things like renting an apartment and applying for and securing a loan for a house or car.

People with low credit scores typically have difficulty repaying loans or making payments on their credit cards, making them unappealing to lenders and merchants alike.

What is a buy now, pay later payment option?

Buy now, pay later (BNPL) platforms work with retailers to offer their customers the option to pay for products in bi-weekly or monthly installments rather than all at once at the time of checkout. Some BNPL providers are interest-free, while some charge varying interest rates depending on the payment plan.

What’s interesting about the BNPL payment model is that it isn’t an entirely new concept. The practice of layaway and payment plans has been around for decades. This practice has been updated for the modern eCommerce marketplace to benefit both the consumer and the merchant.

With BNPL, customers get the item upfront with the understanding that you will make the payments until it is paid off, rather than getting the product when the item is paid off in a layaway format.

BNPL platforms have skyrocketed in popularity for retailers due to several reasons:

- Increase your conversion rate, average order value, and overall sales

- Open your brand to customers who usually would not buy from you due to financial roadblocks

- Reducing shoppers hesitations around making a purchase

- The tech-savviness of Gen Z and their openness to alternative payment methods

Plus, merchants are paid in full and upfront, even with customers on a payment plan, so the risk is minimal.

BNPL solutions like Sezzle empower Gen Zers and Millennials to take control over their credit and spending power. Sezzle currently works with 29k+ active merchants like GameStop, Tobi, and Untuckit and serves a consumer base of ~75% Gen Zers and Millennials.

The benefits of using a buy now, pay later payment option to empower subprime customers financially

Despite subprime consumers often representing a less-desirable consumer segment, there are several benefits of being receptive to reaching this type of customer.

Using a buy now, pay later payment solution, like Sezzle, retailers give customers the ability to purchase and receive items on the spot without having to front the entire cost. With a platform like Sezzle, customers pay in four interest-free equal installments over six weeks.

Plus, as Millennials and Gen Zers enter different life stages, their financial needs evolve. Therefore, their payment preferences are also likely to change.

Let’s take a look at some of the ways retailers can use a BNPL payment method to reach subprime customers in a way that’s impactful for both..

Open your door to a new customer segment

According to the 2019 Consumer Credit Card Market report from the Bureau of Consumer Finance Protection, individuals with a subprime FICO score have a less than 20% chance of being approved for a credit card. Compared to individuals with excellent FICO scores, who have a more than 90% chance of approval, those odds are slim.

Many products and services become inaccessible to subprime consumers without access to a credit card or other loan products. This means lost sales and missed opportunities to build relationships and loyalty, especially with those at the early stage in their financial journey.

Adding a BNPL payment option allows companies to fill the gap left by the traditional credit system. Customers are more likely to make a purchase and add more to their cart if they have the option to pay in installments.

“Most customers would go to their favorite store, see something for a hundred dollars, you know, see that they can break it up into four easy payments, add $50 more [to] their basket because now, it’s more manageable,” says Mia Bernard, Head of Product at Sezzle, in an interview for The Future of Ecommerce podcast. “It gives them more flexibility to do what they want to do with their money that day.”

Making your brand accessible to subprime customers with BNPL paves the way for a long-term relationship.

Position your brand as a win-win financial decision for customers

For customers trying to build their credit, purchasing products on a payment plan may seem too good to be true.

The reality is that younger generations are still trying to figure out how to establish credit. Some of the popular reasons include:

- They haven’t reached a point in life where they want to take out a loan

- They’re trying to recover from past credit mistakes

- They may be skeptical about traditional credit offerings.

Sezzle’s pay-in-four option is an excellent way to turn credit skeptics into credit builders.

A study from Experian found that just 30% of Gen Z consumers have a credit card, and only 19% report having a strong understanding of the fundamentals of credit. Plus, younger consumers prefer debit cards over credit cards—likely because it’s more difficult for them to get approval.

So how can you show subprime customers that shopping with you is a viable way to build credit?

Retailers that use BNPL services give their customers control over their finances. By paying for products in smaller installments, customers can maintain their budgets.

Using a BNPL platform like Sezzle gives you access to tools that help your customers gain control over their credit and teach them how to improve it.

Customers have the option to upgrade to Sezzle Up, Sezzle’s credit-building solution. With Sezzle Up, Sezzle reports customer payment history to the credit bureaus. At Sezzle, we consider individuals with lower credit scores as “prime to be” rather `than subprime. Roughly 80% of Sezzle’s customers would be regarded as subprime by most financial institutions, and over half have a FICO score below 600. Sezzle Up is an excellent option for customers who fit the subprime profile who want to build their credit.

What’s more, customers can continue their financial education with Sezzle Up. We offer guidance, support, and educational resources to increase our customers’ financial literacy.

When customers make payments on time, they improve their credit. Sezzle’s goal is to help customers move out of the subprime status and become qualified for a credit card, which will enhance their spending power. Plus, as customers continue to complete payments on time, their Sezzle Limit increases, enhancing their buying power.

Sounds like a win-win, right?

Keep up with the changing retail landscape

2020 was a year that drastically changed consumer behavior. Both brick-and-mortar retailers and eCommerce merchants have had to make adjustments based on the repercussions of the pandemic. From contactless payments and curbside pickup to increased concern around store hygiene and protocols, retailers must keep up with retail’s changing tides.

Another notable change that’s shaken up the retail industry is the declining use of credit cards. According to the Federal Reserve Bank of New York, the number of credit application rates dropped by 11%, and rejection rates increased on average by 3.8%.

With unpredictable income and wavering job security plaguing the economy due to the coronavirus, BNPL methods are an excellent way for consumers to purchase the things they want (and need!) while boosting their credit and spending power.

There’s an opportunity for growth among subprime consumers who want to build their credit

Subprime consumers are a viable market to tap into despite their “bad” reputation. It’s an excellent market for boosting your bottom line, building a new customer base, and positioning your brand as one that encourages financial growth and health.

Ready to get started with buy now, pay later software? Sign up for Sezzle today.